Multi-commerce channel wallet for authenticated transactions

a multi-channel, wallet technology, applied in the field of transactions for payment of goods/services, can solve the problems of different levels of fraud risk associated, greater risk of financial fraud, and risk of financial fraud, and achieve the effects of reducing the implementation requirements of merchants, reducing fees, and improving economics

- Summary

- Abstract

- Description

- Claims

- Application Information

AI Technical Summary

Benefits of technology

Problems solved by technology

Method used

Image

Examples

Embodiment Construction

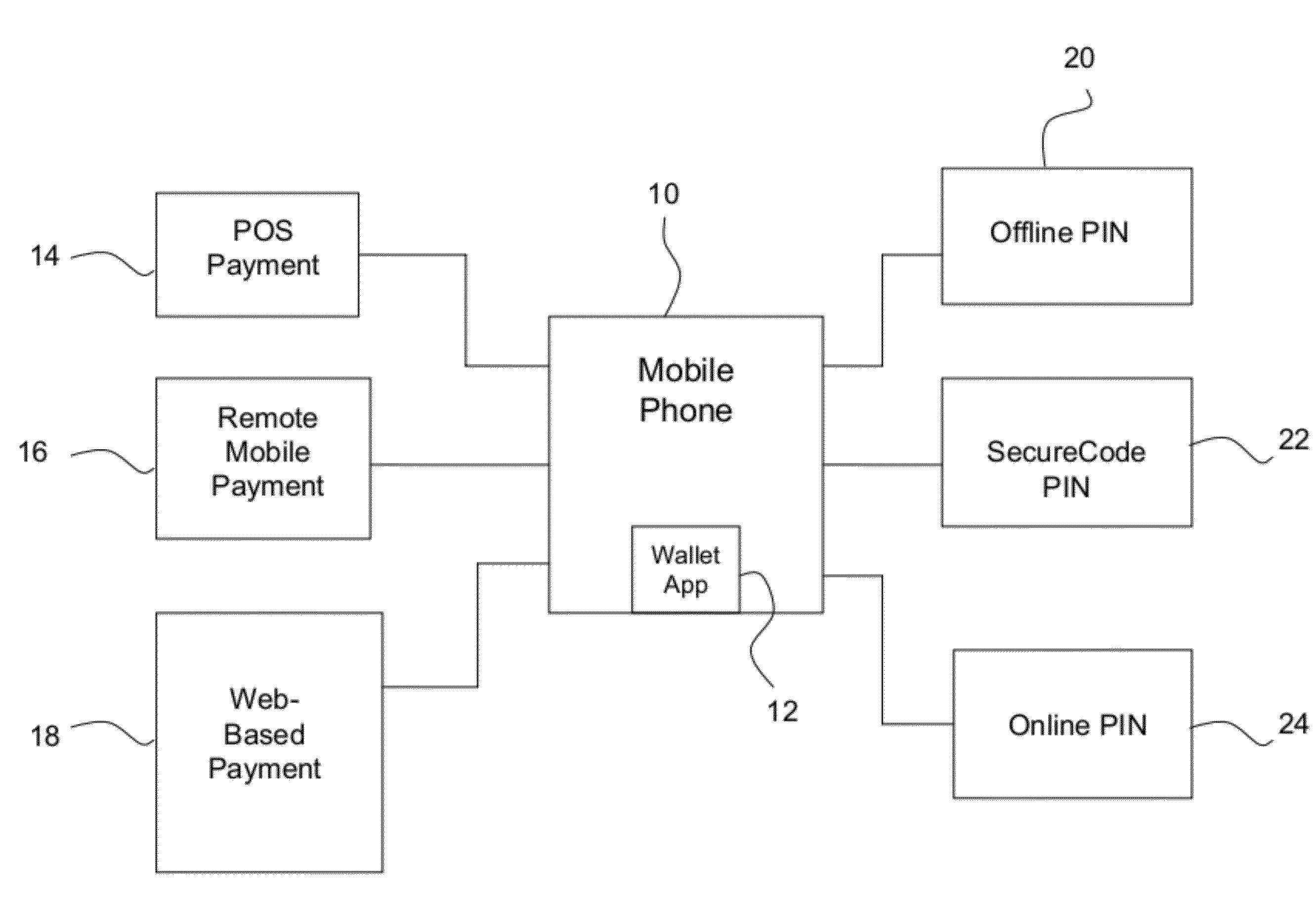

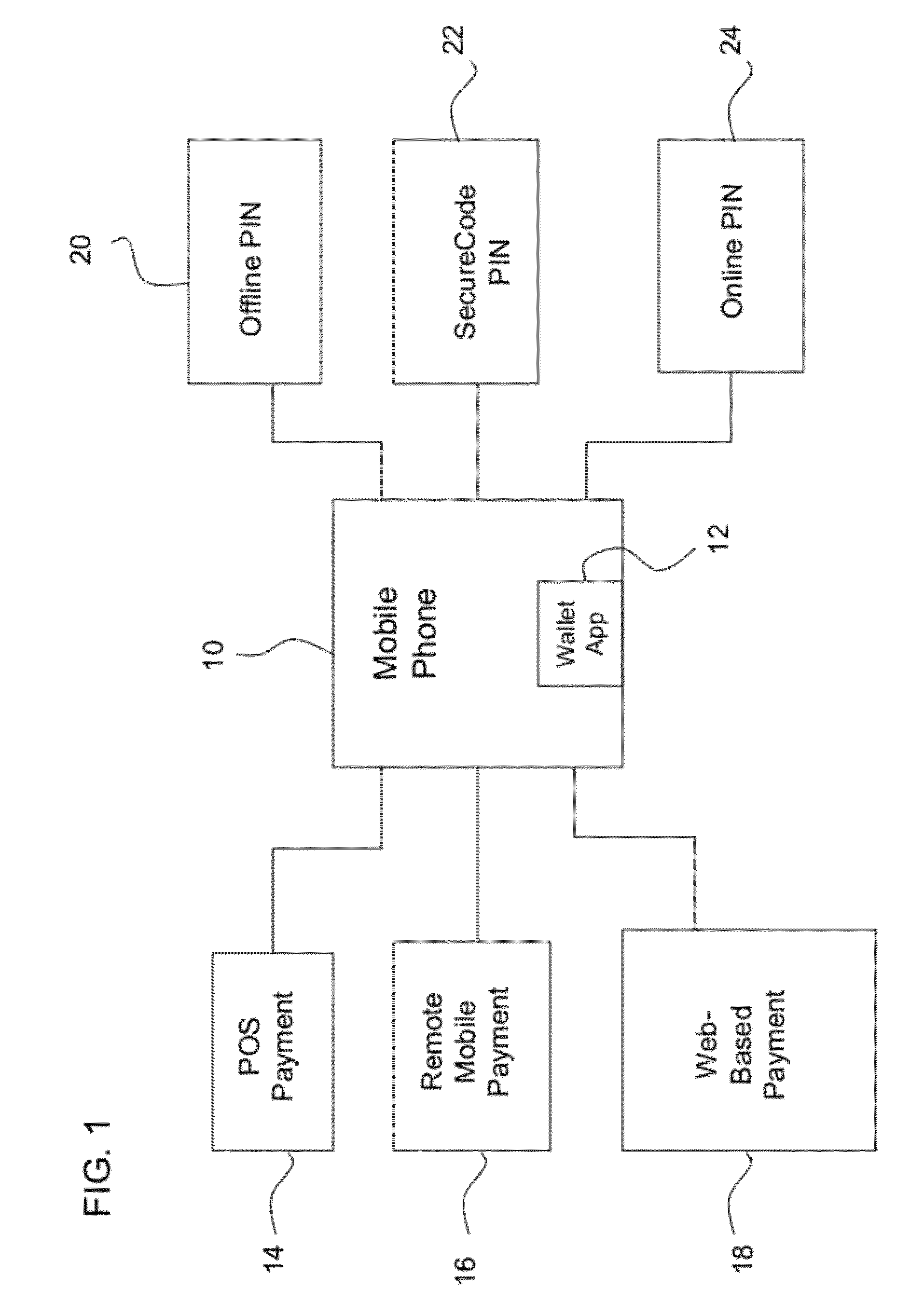

[0024]Referring now to FIG. 1, the present invention is centered around a mobile phone 10 associated with a payment card, e.g., a credit card, debit card or prepaid card. The mobile phone is preferably capable of storing and / or running a wallet application 12, which is preferably a browser-based mobile application capable of storing selected information such as a cardholder name, card alias, billing / shipping address, etc., locally on the phone or in a cloud server. In one preferred embodiment, the mobile phone is a “smart phone”, and the wallet application is stored in a memory device located in the phone. It is contemplated herein that the system and method of the present invention will enable payments across multiple channels of commerce, e.g., a POS payment 14 by, for example, a PayPass terminal, a remote mobile payment 16 initiated by a mobile phone, and / or a web-based payment 18.

[0025]As further described in FIG. 1, the present invention contemplates the use of various authenti...

PUM

Login to View More

Login to View More Abstract

Description

Claims

Application Information

Login to View More

Login to View More - R&D

- Intellectual Property

- Life Sciences

- Materials

- Tech Scout

- Unparalleled Data Quality

- Higher Quality Content

- 60% Fewer Hallucinations

Browse by: Latest US Patents, China's latest patents, Technical Efficacy Thesaurus, Application Domain, Technology Topic, Popular Technical Reports.

© 2025 PatSnap. All rights reserved.Legal|Privacy policy|Modern Slavery Act Transparency Statement|Sitemap|About US| Contact US: help@patsnap.com